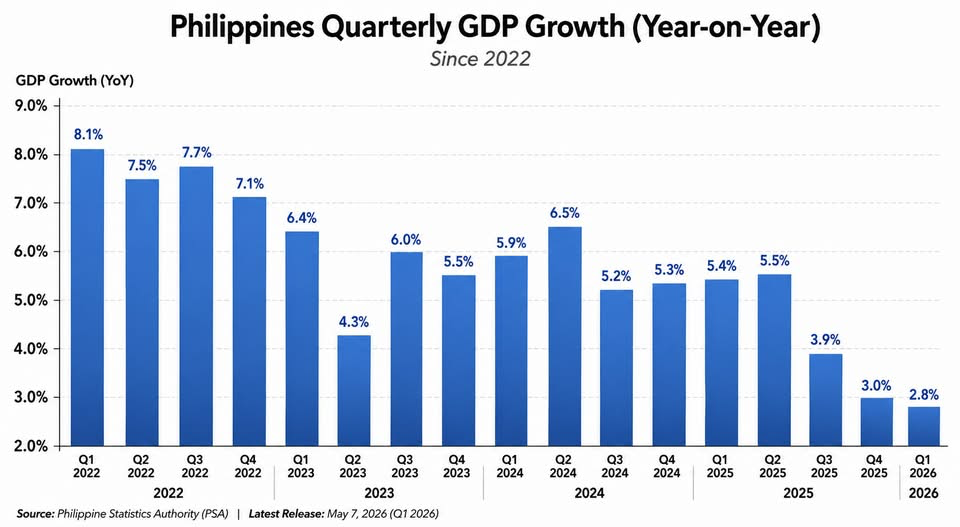

From 8.1% growth in Q1 2022, GDP has fallen to just 2.8% in Q1 2026, the weakest since the COVID recession. This is no longer a simple post-pandemic normalization. It is a warning sign.

The actual outcome was even weaker than the already pessimistic forecasts of BusinessWorld and below the lower end of the government’s 5% to 6% growth target.

Worse, the quarter did not yet fully capture the impact of the Iran and Middle East crisis because the war only began on February 28. Much of the oil shock, transport disruption, inflationary pressure, and investor uncertainty will be felt more heavily in the succeeding quarters.

Now inflation is surging at 7.2%. If the BSP raises interest rates to fight inflation, borrowing becomes more expensive, investment weakens, consumption slows, and job creation suffers.

That creates a vicious cycle. Weak growth reduces revenues. Higher rates raise debt-service costs. Slower job creation squeezes households. All of this comes while the Philippines is already carrying an excessive debt-to-GDP burden.

This is the danger zone. Weak growth. High inflation. Expensive debt. Fewer jobs.

The government cannot keep selling “resilience” when the numbers are already screaming stagnation.